Use your Visa or MasterCard to make a donation to the American Red Cross, a local nonprofit, or even to help feed the hungry and the banks also gets a cut. There is no negotiating on interchange fees. If a wealthy contributor uses a premium affinity card, which merits free airline miles, then not just the donor, but the charity is also taken on a ride.

From just one story shared with us: After toiling for weeks to prepare for a major gala fundraiser which raised nearly $50,000 for a nonprofit organization, the bank-owned credit card associations also attended the affair - in a big way. An associate from a local foundation explained that their directors were livid when the bill came due. After all the work invested to raise the much needed funding, about $1,200 was taken off the top to pay for the bank interchange fees. Remember, this was a nonprofit which had to pay the banks in order to provide a card payment option.

Because foundations understand that convenience and simplicity help expedite contributions, they must accept Visa and MasterCard. However, unlike all the other service providers, they are unable to negociate their rates. What the donors and organizations may not realize is that a high percent of the proceeds are paid in interchange fees. For automatic monthly donations, an interchange fee is paid every month. For non-electronic transactions which require manual card imprints, the fee could be four or five percent of the total transaction. Or, much greater when premium cardholders contribute.

In this case, the bank offered the group free checking and free use of the credit card equipment, but they still charged about $1,200. Think of how vital $1,200 would have been for the nonprofit and how it instead was used to fund the banks multibillion dollar interchange scheme. But, the bank was benevolent. They did offer the group free checking, which may otherwise cost, what, five-dollars a month? And, they kicked in a free card terminal. Freakishly, that almost sounds like what an unscrupulous person selling illegal drugs might do; provide free needles but charge for the fix.

Last Summer, immediately after the Hurricane Katrina disaster, we contacted MasterCard and Visa’s CEO to request that they rescind the interchange fees for donations to the relief efforts, as otherwise the banks were profiteering from this national calamity. In the same request was a plea to also rescind the interchange fees motorists pay when filling up their cars. Gas prices had doubled and threatened our economy. Why should Visa and MasterCard have reaped windfall profits and taken advantage of our fiscally ruinous energy crisis? Just as with donations to non profits, the banks were silent in action on arresting interchange fees for these categories.

[source: WayTooHigh.com]

Friday, March 31, 2006

Wednesday, March 29, 2006

30 Minute Photos Etc.® (lead plaintiff) Profile (Photo Trade News)

Photo Trade News® , by Jerry Lansky, Excerpt:

Every industry has its “go-to” guy. Whenever we talk about a moon shot, Walter Cronkite is called on to comment. When it’s a matter of international relations, it’s Henry Kissinger (though of late, retired newsman Dan Rather is frequently sought for an opinion).

The retail photo processing industry has its own spokesman of sorts. Maybe not with quite the global stature of the aforementioned, but without the grey hair. It seems as though when there’s a newspaper or magazine article having to do with on-site processing, chances are you’ll see him being quoted as an industry spokesman.

Our industry go-to is Mitch Goldstone. His name pops up in The Wall Street Journal, The New York Times, LA Times, wire services, magazines, and other media. When there’s a hot topic, Mitch gets called. Sometimes he initiates the call to express his opinion—of which he has many. Then there are Mitch’s somewhat quixotic pursuits, like the current one in which he is the lead complainant in a multibillion-dollar suit against Visa, MasterCard, and some large banks. The entire retail world, including the U.S. government (which has a $100 million stake in the suit), hopes he succeeds.

[source: Photo Trade News® , March 2006]

Tuesday, March 28, 2006

Amex® / MasterCard® co-branded Cards (WayTooHigh.com

Westpac® , and Australian-based bank is issued a dual-branded Amex® / MasterCard® . When a retailer does not accept American Express® , the card would be used as a MasterCard® . Australia's leading paper, The Herald Sun described how the card will work, but as with other commentaries on these new American Express® co-branded card, the question surrounding interchange fees remains unanswered.

[source: WayTooHigh.com, as read in The Herald Sun, March 28]

[source: WayTooHigh.com, as read in The Herald Sun, March 28]

Washington Mutual's® "Free Checking" (WayTooHigh.com)

Washington Mutual® , a named defendant in the antitrust price-fixing litigation, is promoting a new campaign for what it calls "Free Checking." What else is free are the interchange charges when writing checks, which unlike electronic payment transactions, face the economic burden of clearinghouse and other payment costs. The Washington Mutual® marketing campaign draws attention to the question of why there are interchange fees for credit and debit card transactions, yet none for writing checks?

[source: WayTooHigh.com]

[source: WayTooHigh.com]

Monday, March 27, 2006

"Court Battle Looms Over Credit Card 'Hidden Tax'" (Competition Law 360)

"Fed up with what they consider a “hidden tax” for merchants and consumers by credit card companies and their banks, merchants have decided to fight back with a large-scale antitrust class-action lawsuit against the major credit card companies. But past court decisions that have sided with the credit card companies could prove a significant challenge for the merchants as they fight their way through court."

[subscription required]

[subscription required]

Saturday, March 25, 2006

Friday, March 24, 2006

"Mexican Banks Cut Credit Card Fees by $200 Million" (Bloomberg)

On March 23rd, Bloomberg reported that Citigroup Inc. and other banks in Mexico agreed to again lower the merchant interchange fees for the second time in as many years. Up until the recent antitrust litigation against Visa and MasterCard, the U.S. trend was to regularly raise rates with unbridled arrogance.

Under a year ago, the banks which control Visa and MasterCard again raised rates in the U.S.. MasterCard elevated its merchant fees when cardholders pulled its premium World cards from their wallets and Visa raised its rate for their high-end Signature cards.

The new weighted-average interchange in Mexico is about the rate charged by banks in the U.S. Interchange, which was designed to be cost based for processing electronic payment transactions, is now a $25 billion dollar annual bank windfall. A study of the U.S. market, where technology leads the world for faster, more efficient electronic transactions and where fraud costs are subpar with Mexico is one example. With today's news, Visa and MasterCard will be grasping to maintain their fiefdom. WayTooHigh.com can already imagine those full-page advocacy ads that might be planned for the financial papers proclaiming a bent story on why these fees are necessary.

Mexican Interchange fees for credit cards will be about 1.8% and .80% for debit cards. While the Federal Reserve System in the U.S. watches, Mexico's Central Bank boldly "criticized the fees that banks levy on consumers and merchants" during a bankers meeting in 2005, as reported by Bloomberg.

Banks based outside Mexico control 90% of that nation's financial system.

Click here for more info.

[Source: WayTooHigh.com]

Under a year ago, the banks which control Visa and MasterCard again raised rates in the U.S.. MasterCard elevated its merchant fees when cardholders pulled its premium World cards from their wallets and Visa raised its rate for their high-end Signature cards.

The new weighted-average interchange in Mexico is about the rate charged by banks in the U.S. Interchange, which was designed to be cost based for processing electronic payment transactions, is now a $25 billion dollar annual bank windfall. A study of the U.S. market, where technology leads the world for faster, more efficient electronic transactions and where fraud costs are subpar with Mexico is one example. With today's news, Visa and MasterCard will be grasping to maintain their fiefdom. WayTooHigh.com can already imagine those full-page advocacy ads that might be planned for the financial papers proclaiming a bent story on why these fees are necessary.

Mexican Interchange fees for credit cards will be about 1.8% and .80% for debit cards. While the Federal Reserve System in the U.S. watches, Mexico's Central Bank boldly "criticized the fees that banks levy on consumers and merchants" during a bankers meeting in 2005, as reported by Bloomberg.

Banks based outside Mexico control 90% of that nation's financial system.

Click here for more info.

[Source: WayTooHigh.com]

Thursday, March 23, 2006

Interchange Wars: Empowering Entrepreneurs to Battle the Banks (WayTooHigh.com)

Can an individual change the world? Just think of Margaret Mead's famed quote: "Never Doubt That A Small Group of Thoughtful Committed Citizens Can Change The World: Indeed It's The Only Thing That Ever Has."

"An Army of David's," written by Glenn Reynolds explains how markets and technology empower ordinary people to beat big media, big government, and other goliaths. WayTooHigh.com - The Credit Card Interchange Report is but one example of how customers are fighting back against what we alledge are illegal price-fixing practices by Visa, MasterCard and its member banks.

[source: WayTooHigh.com]

"An Army of David's," written by Glenn Reynolds explains how markets and technology empower ordinary people to beat big media, big government, and other goliaths. WayTooHigh.com - The Credit Card Interchange Report is but one example of how customers are fighting back against what we alledge are illegal price-fixing practices by Visa, MasterCard and its member banks.

[source: WayTooHigh.com]

MasterCard International Offers 'Peace of Mind,' But Still Gets Piece of Wallet (WayTooHigh.com

A March 23th, Business Wire release issued by MasterCard International announced that it will offer certain cards designed for small business cardholders with new fraud protection.

The bank-owned card association announced it is "extending its zero liability policy to U.S.-issued MasterCard BusinessCard®) and Debit MasterCard BusinessCard®) cards. Beginning in September, those small business debit and cardholder customers will not be liable due to unauthorized use of their cards.

The irony is MasterCard calls this "‘peace' of mind," yet the billions in profits from unbridled merchant interchange fees paid by these very same small businesses is anything but peaceful. In one hand, the company promotes "peace of mind," yet the reality is they are demanding a piece of the wallet and a large portion at that. The U.S. interchange rates demanded by MasterCard (and Visa) are more than twice the fee charged in many other nations. And, some countries, like Canada have a zero interchange fee for PIN debit cards.

The press release explained this new "zero liability protection" was designed to help give "small business owners 'peace of mind' so they can focus on growing their business."

If MasterCard was indeed interested in helping small, emerging, mid and multinational-sized businesses with more assistance, then they would start at home by recognizing that interchange fees are an antiquated artifact which were designed decades ago when retailers used cumbersome, manual credit card imprinters and minimal technology required this once cash-based fee.

[source: WayTooHigh.com]

The bank-owned card association announced it is "extending its zero liability policy to U.S.-issued MasterCard BusinessCard®) and Debit MasterCard BusinessCard®) cards. Beginning in September, those small business debit and cardholder customers will not be liable due to unauthorized use of their cards.

The irony is MasterCard calls this "‘peace' of mind," yet the billions in profits from unbridled merchant interchange fees paid by these very same small businesses is anything but peaceful. In one hand, the company promotes "peace of mind," yet the reality is they are demanding a piece of the wallet and a large portion at that. The U.S. interchange rates demanded by MasterCard (and Visa) are more than twice the fee charged in many other nations. And, some countries, like Canada have a zero interchange fee for PIN debit cards.

The press release explained this new "zero liability protection" was designed to help give "small business owners 'peace of mind' so they can focus on growing their business."

If MasterCard was indeed interested in helping small, emerging, mid and multinational-sized businesses with more assistance, then they would start at home by recognizing that interchange fees are an antiquated artifact which were designed decades ago when retailers used cumbersome, manual credit card imprinters and minimal technology required this once cash-based fee.

[source: WayTooHigh.com]

Friday, March 17, 2006

Citigroup® , Bank of America® and HSBC® scheme with American Express (WayTooHigh.com)

(Republished) Latest banking trick: Imprint the American Express® logo on millions of new credit cards and charge in some cases more than double current merchant interchange fees.

As co-editors of The Credit Card Interchange Report - WayTooHigh.com, we are sensitive to our parallel but indirect roles as lead plaintiffs in one of largest antitrust litigations in our nation's history. However, we have a question for Citigroup® , Bank of America® and HSBC which is shared by many retailers, consumers and the media.

We use this forum because the banks and many of their agents, including advocacy, public relations and legal firms are regular readers of The Credit Card Interchange Report - WayTooHigh.com.

Perhaps, one of them can answer this question: What are the planned interchange fees associated with the pack of new American Express® -branded cards to be introduced in 2006?

We also address this question to American Express® , where 62% of the company's revenues are derived from merchant interchange fees.

[Earlier this week, the New York financial-services company settled another class-action lawsuit over hidden foreign currency transaction fees. American Express explained that it was better to pay out $75 million and "avoid the costs and risks of prolonged litigation."]

Already faced with one of the industrialized nations highest interchange charges, U.S. retailers are aghast at the recent announcement by Citigroup® , Bank of America® and the British banking giant, HSBC Holdings Plc® . The three leading banks will soon market millions of American Express® -branded charge cards.

Will a simple change to the logo on charge cards maintain the existing way too high Visa® and MasterCard® interchange fees, or will it be even higher as retailers and consumers are forced to bare a nearly 3, 4 or 5-percent fee that is charged by American Express® ?

With ultra-competitive margins, if a retailer has a 2-3% return on investment (ROI), this means with millions of new American Express® -logoed cards that the ROI is diminished and profitability decimated.

[source: WayTooHigh.com]

As co-editors of The Credit Card Interchange Report - WayTooHigh.com, we are sensitive to our parallel but indirect roles as lead plaintiffs in one of largest antitrust litigations in our nation's history. However, we have a question for Citigroup® , Bank of America® and HSBC which is shared by many retailers, consumers and the media.

We use this forum because the banks and many of their agents, including advocacy, public relations and legal firms are regular readers of The Credit Card Interchange Report - WayTooHigh.com.

Perhaps, one of them can answer this question: What are the planned interchange fees associated with the pack of new American Express® -branded cards to be introduced in 2006?

We also address this question to American Express® , where 62% of the company's revenues are derived from merchant interchange fees.

[Earlier this week, the New York financial-services company settled another class-action lawsuit over hidden foreign currency transaction fees. American Express explained that it was better to pay out $75 million and "avoid the costs and risks of prolonged litigation."]

Already faced with one of the industrialized nations highest interchange charges, U.S. retailers are aghast at the recent announcement by Citigroup® , Bank of America® and the British banking giant, HSBC Holdings Plc® . The three leading banks will soon market millions of American Express® -branded charge cards.

Will a simple change to the logo on charge cards maintain the existing way too high Visa® and MasterCard® interchange fees, or will it be even higher as retailers and consumers are forced to bare a nearly 3, 4 or 5-percent fee that is charged by American Express® ?

With ultra-competitive margins, if a retailer has a 2-3% return on investment (ROI), this means with millions of new American Express® -logoed cards that the ROI is diminished and profitability decimated.

[source: WayTooHigh.com]

Thursday, March 16, 2006

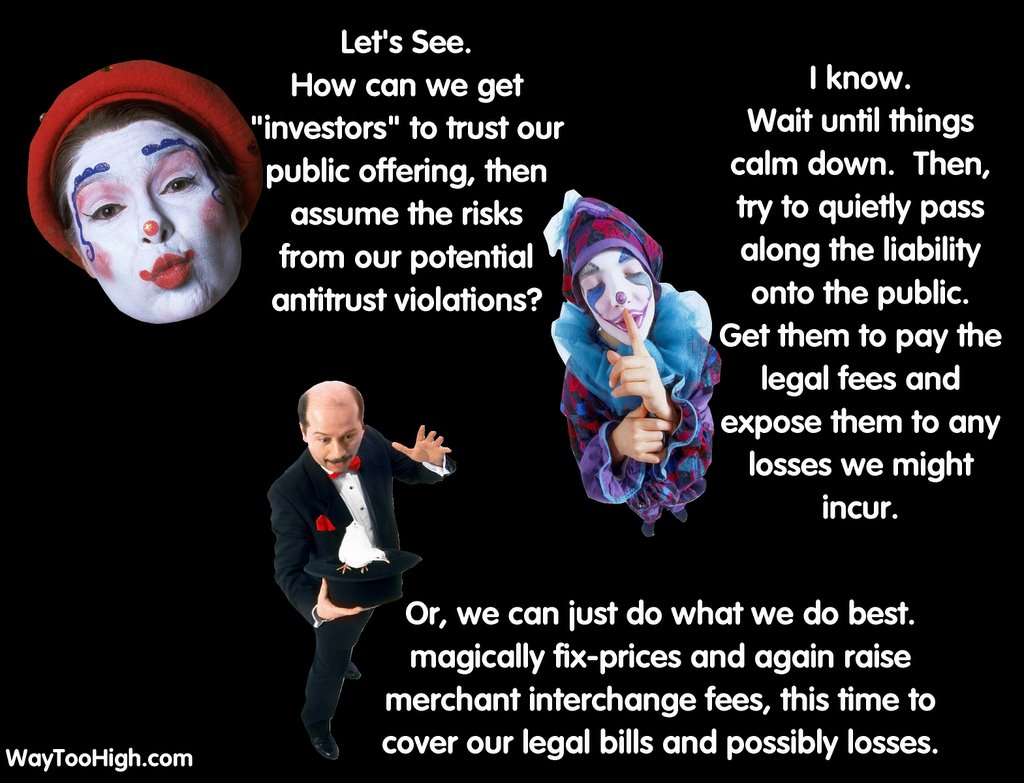

Company Planning Largest IPO Since Google, Reports Quarterly Loss (WayTooHigh.com)

MasterCard Inc. while continues to plan for a 2nd quarter IPO and what would be the largest offering since Google's 2004 financing, reported 4th quarter sales. Sales during the key holiday retail season was not enough to turn a profit at the nation's second largest credit card association, as MasterCard Inc. reported a 4th quarter loss of more than $50 million.

Even though MasterCard continues to suggest that the public will embrace its public offering sometime prior to the end of June, investors will have a hard time skirking the liability from the multi-billion dollar antitrust interchange litigation.

Click here for more info

[Source: WayTooHigh.com]

Tuesday, March 14, 2006

"If You Cannot Argue The Facts..." (WayTooHigh.com)

A recent guest commentary in the Silicon Valley/San Jose Business Journal, argues all types of pro-banking reasons to support what many see as a $25 billion annual hidden interchange tax on retailers and merchants. What was missing was any reference to the law and discussion of why the United States antitrust, price-fixing regulations are so important. Click here to view the complaint and understand the facts.

[source: WayTooHigh.com]

[source: WayTooHigh.com]

Monday, March 13, 2006

Consumer group opposes Capital One-North Fork deal (Reuters)

Click here to view the Reuters story on a challenge to the Capital One Financial Corp. proposed acquisition of North Fork Bancorp Inc.

[source: Reuters]

[source: Reuters]

The Mission: WayTooHigh.com

With daily visitors from across the globe, WayTooHigh.com - The Credit Card Interchange Report has become the most comprehensive, daily chronicler of news and commentary on the history of merchant interchange fees.

Our goal in representing millions of merchants and cardholders is to reform an antiquated, costly and unfair payment system and explain why the $25 billion annual merchant interchange fee is a hidden tax on consumers.

Personally, the heart behind this website is our passion for civic activism and supporting important causes. There also is a real company behind this website - 30minphotos.com, founded in 1990 and based in Irvine, California.

At times is has been challenging to run our retail and national online boutique photo service along with the demands for propagating this website. But, the value in packaging of and commenting on merchant interchange is necessary.

Are we also running a commercial business? Absolutely, and that is the foundation for our personal knowledge on interchange. Are we authentic? You bet.

Our mission has a strong point of view, but our visibility is helping to draw attention and we are in good company. There are few occasions when all-sized businesses join together on an issue. Do we think our goal to force the bank-owned credit card associations to reevaluate their interchange fees will be successful? We hope so.

This pause from our regular updates was provided to also extend our appreciation for your readership.

Mitch Goldstone and Carl Berman - co-editors, WayTooHigh.com - The Credit Card Interchange Report.

[source: WayTooHigh.com]

Sunday, March 12, 2006

Further Wave of Consolidation in Credit Card Industry Worries Retailers (WayTooHigh.com)

One of the largest credit-card issuers is getting even larger and draws more attention to anticompetitive attrition within the credit-card industry.

The Wall Street Journal's online edition late Sunday reported that Capital One is preparing to acquire the regional bank holding company, North Fork Bancorp for about $14.5 Billion. WSJ reporters, Dennis Berman and Robin Sidel wrote that this brings "the large credit-card issuer deeper into the banking business."

With a further consolidation in the banking and credit card industry, WayTooHigh.com anticipates that there will be a further reduction of competition and as a result, the possibility of higher interchange fees.

More info click here, WSJ subscription required

More on North Fork Bancorp, click here

[source: WayTooHigh.com, reporting on the WSJ news alert]

The Wall Street Journal's online edition late Sunday reported that Capital One is preparing to acquire the regional bank holding company, North Fork Bancorp for about $14.5 Billion. WSJ reporters, Dennis Berman and Robin Sidel wrote that this brings "the large credit-card issuer deeper into the banking business."

With a further consolidation in the banking and credit card industry, WayTooHigh.com anticipates that there will be a further reduction of competition and as a result, the possibility of higher interchange fees.

More info click here, WSJ subscription required

More on North Fork Bancorp, click here

[source: WayTooHigh.com, reporting on the WSJ news alert]

Card & Payments Magazine Features Interchange Commentary by Mitch Goldstone

Click here to view the March, 2006 "Afterthoughts" Card & Payments Magazine commentary written by Mitch Goldstone, lead plaintiff in the interchange antitrust litigation.

[source: Cards & Payments] (pfd format)

[source: Cards & Payments] (pfd format)

Saturday, March 11, 2006

NACS President Blasts Credit-Card Fees (Convenience Store News)

NACS President Blasts Credit-Card Fees

ALEXANDRIA, Va. (3-11-06) -- Henry O. Armour, president and CEO of the National Association of Convenience Stores, testified before the House Energy and Commerce Committee’s Subcommittee on Commerce, Trade and Consumer Protection on the industry’s long struggle with credit-card interchange fees, reported NACSOnline."

Interchange fees are levied in a market that is broken and something must be done to fix it," Armour said. "This hearing is an important step toward informing Congress and the public about the impact that high interchange rates have on U.S. consumers.

There has not been nearly enough information and discussion about these fees in the past, and we applaud you for your willingness to examine them." NACS was invited to testify as a result of its testimony in September 2005 before the full Committee regarding gasoline prices and the increasing amount of money that credit-card companies take out of every gallon of gasoline purchased, reported NACSOnline.

Armour outlined in the report four fundamental problems with the current interchange market. First, he noted that due to the market power of the card associations, retailers have no choice about whether they accept cards. Second, the card associations exploit their market power by driving up fees and by veiling these fees and their rules in secrecy. Third, these fees are bad for consumers -- particularly some middle- and many lower-income consumers who do not have easy access to credit and debit cards. And fourth, consumers in the United States pay much more for interchange than other comparable countries.

Most consumers have no idea that they pay interchange fees, which are hidden in the price of virtually everything they buy and total an estimated $27 billion annually in the United States, according to NACS. Consumers do not know about these hidden fees because the credit card companies go through great lengths to assure that consumers remain in the dark about these fees, Armour said in the report."

It's not just consumers who are left in the dark; Visa and MasterCard refuse to fully disclose their operating rules to retailers," Armour said. " It is remarkable that they make retailers agree to abide by all of their operating rules in order to be able to accept their cards."Ultimately, consumers pay the price. According to NACS, the average American family pays $331 in interchange and related fees every year. And that is true whether or not that family uses credit or debit cards. Because these fees are hidden in the cost of virtually everything consumers buy, even cash-paying consumers ultimately pay for them, according to NACSOnline."

This results in a nasty, regressive charge," Armour said. "Consumers with fewer resources whose credit does not allow them to have credit cards or do not have debit cards pay this fee like everyone else -- as do consumers with credit cards who pay high interest rates, annual fees and have no rewards or miles programs."

[source: Convenience Store News]

Wednesday, March 08, 2006

Shouldn't Technology Yield Lower Interchange Fees? (WayTooHigh.com)

During a recent exchange with a senior executive VP at a major bank, they explained that payment card fraud costs justified soaring Interchange fees. [Actually, "soaring" is my word, but the point does warrant a closer examination].

A recent WayTooHigh.com posting referenced Moore's Law, where technology causes lower prices and faster service.

Visa international has an entirely brilliant new payment solution which plays into Moore's Law and our argument that Interchange fees are no longer necessary. As reported in the March edition of "Cards & Payments Magazine," which included a guest commentary by Mitch Goldstone (page 56), display card authorization helps protect the integrity of electronic transactions. Visa is working to embed an electronic code within the cards. Click here to view one product which uses code encrypting.

"A Cardholder would generate the code by pressing the Visa logo on the card's front. A digital box in the upper right corner would display the number. The pass code would be stored in the merchant's or financial institution's database tied to the consumer's card or password," reported Cards & Payment. A matching code would be verified by the merchants electronic terminal and help remedy questionable transactions and further reduce the need for interchange charges.

[source: WayTooHigh.com]

A recent WayTooHigh.com posting referenced Moore's Law, where technology causes lower prices and faster service.

Visa international has an entirely brilliant new payment solution which plays into Moore's Law and our argument that Interchange fees are no longer necessary. As reported in the March edition of "Cards & Payments Magazine," which included a guest commentary by Mitch Goldstone (page 56), display card authorization helps protect the integrity of electronic transactions. Visa is working to embed an electronic code within the cards. Click here to view one product which uses code encrypting.

"A Cardholder would generate the code by pressing the Visa logo on the card's front. A digital box in the upper right corner would display the number. The pass code would be stored in the merchant's or financial institution's database tied to the consumer's card or password," reported Cards & Payment. A matching code would be verified by the merchants electronic terminal and help remedy questionable transactions and further reduce the need for interchange charges.

[source: WayTooHigh.com]

Monday, March 06, 2006

MasterCard 'priceless' ad serves do-it-yourself comedic levity for retailers (WayTooHigh.com)

MasterCard International surely did not plan for its core customers to laugh and have fun at their expense by typing what they really feel, but... Sunday evening's Academy Awards (R) featured several MasterCard International "fill in-the-blank" spots that are easy to spoof.

Viewers were prompted to visit Priceless.com and enter a contest. The comical side is that when you visit the site you can type in the word "interchange" and then view the recast commercial with the text you just entered. Merchants who face this annual $25 billion fee and consumers who pay this hidden tax with each charge and debit card purchase may find some humor in viewing the freshly designed spots.

Afterwards, you can even forward the link from your custom-designed commercial for others to watch too.

[Update: BrandWeek reported that 100,000 consumers responded to the contest]

[source: WayTooHigh.com]

Viewers were prompted to visit Priceless.com and enter a contest. The comical side is that when you visit the site you can type in the word "interchange" and then view the recast commercial with the text you just entered. Merchants who face this annual $25 billion fee and consumers who pay this hidden tax with each charge and debit card purchase may find some humor in viewing the freshly designed spots.

Afterwards, you can even forward the link from your custom-designed commercial for others to watch too.

[Update: BrandWeek reported that 100,000 consumers responded to the contest]

[source: WayTooHigh.com]

Saturday, March 04, 2006

MasterCard's® New Interactive 'Price-less' Ads ® (WayTooHigh.com)

Sometimes, you just get the perfect softball pitch that provokes a reply.

WayTooHigh.com - The Credit Card Interchange Report just saw this one coming in slow motion. The answer to the new "Write Your Own MasterCard Ad" is ... "Interchange."

In February, we drew attention to Visa's® sponsorship of the Winter Games by focusing on the question of why interchange rates were half the rate in Italy. Now, as Sunday's Oscars (R) gears up to celebrate the best in Hollywood cinema, the spotlight is on MasterCard. The second largest card issuer will broadcast two commercials.

The card issuer's campaign encourages viewers to visit MasterCard International's® priceless.com® site to enter a contest. AdWeek® commented that "after 8-years of `priceless' moments" consumers will be able to fill in the blanks." This largely is what the Federal antitrust litigation against MasterCard® is about too. As lead plaintiff battling MasterCard® , we couldn't have produced a more direct and effective campaign to draw attention to interchange. Asking to fill in the blanks spotlights how the bank-owned card association illegally fix prices, forcing consumers and merchants to pay whatever rates they mandate. Ironically, the commercials ask consumers to identify the items that relate to various prices. Most people draw blanks when it comes to knowning what interchange fees are paid for each charge transaction.

Just think of those prices as hidden interchange fees which retailers and consumers have no choice but to pay due to the price-fixing, collusive bank practices.

The two MasterCard® spots will depart from the traditional identification of a product or service and the corresponding price. Instead, there will be a contest to identify the items that relate to various prices - the option of possibilities to choose from is endless.

Choosing which words will appear in the finished copy of a future ad is the contest; the winning selection will be broadcast later this year by MasterCard® . As more people become familiar with the $25 billion annual merchant interchange fees and hidden tax on consumers, the best answer to fill in the blank is ... "Interchange."

In a sharp departure from what MasterCard® must have thought was a creative advertisement, retailers who tune in on the Sunday awards show will immediately recognize that the unambiguous answer are the interchange fees, especially when the announcer says : "blank, blank, blank" because with nearly one-hundred interchange rate structures, the possibilities are endless.

Imagine if cardholders and retailers visited the priceless.com website and selected as their contest entry the word "interchange." That would be a priceless message to MasterCard® .

[source: WayTooHigh.com]

WayTooHigh.com - The Credit Card Interchange Report just saw this one coming in slow motion. The answer to the new "Write Your Own MasterCard Ad" is ... "Interchange."

In February, we drew attention to Visa's® sponsorship of the Winter Games by focusing on the question of why interchange rates were half the rate in Italy. Now, as Sunday's Oscars (R) gears up to celebrate the best in Hollywood cinema, the spotlight is on MasterCard. The second largest card issuer will broadcast two commercials.

The card issuer's campaign encourages viewers to visit MasterCard International's® priceless.com® site to enter a contest. AdWeek® commented that "after 8-years of `priceless' moments" consumers will be able to fill in the blanks." This largely is what the Federal antitrust litigation against MasterCard® is about too. As lead plaintiff battling MasterCard® , we couldn't have produced a more direct and effective campaign to draw attention to interchange. Asking to fill in the blanks spotlights how the bank-owned card association illegally fix prices, forcing consumers and merchants to pay whatever rates they mandate. Ironically, the commercials ask consumers to identify the items that relate to various prices. Most people draw blanks when it comes to knowning what interchange fees are paid for each charge transaction.

Just think of those prices as hidden interchange fees which retailers and consumers have no choice but to pay due to the price-fixing, collusive bank practices.

The two MasterCard® spots will depart from the traditional identification of a product or service and the corresponding price. Instead, there will be a contest to identify the items that relate to various prices - the option of possibilities to choose from is endless.

Choosing which words will appear in the finished copy of a future ad is the contest; the winning selection will be broadcast later this year by MasterCard® . As more people become familiar with the $25 billion annual merchant interchange fees and hidden tax on consumers, the best answer to fill in the blank is ... "Interchange."

In a sharp departure from what MasterCard® must have thought was a creative advertisement, retailers who tune in on the Sunday awards show will immediately recognize that the unambiguous answer are the interchange fees, especially when the announcer says : "blank, blank, blank" because with nearly one-hundred interchange rate structures, the possibilities are endless.

Imagine if cardholders and retailers visited the priceless.com website and selected as their contest entry the word "interchange." That would be a priceless message to MasterCard® .

[source: WayTooHigh.com]

Friday, March 03, 2006

"Free" Travel Awards Cost Merchants (WayTooHigh.com)

If a customer earlier today at 30minphotos.com was accurate, they wanted our retail and online boutique photo center to complete their debit card transaction as a signature credit card so they could accrue airline mileage. Even though it was a debit card and their account would instantly be deducted by that transaction, we scanned the card at the much higher percent-of-sale rate so the customer could earn mileage; the transaction cost us several dollars rather than just about 50-cents.

If this is accurate, the credit card issuers are conditioning consumers to force retailers to pay substantially higher interchange fees. By using the allure of frequent flyer awards, the cardholders become Visa and MasterCard's moll to further enrich the multi-billion dollar interchange scheme. The banks promote the use of debit cards to help consumers budget their money, but the result is that merchants then are asked to process the card at much higher rates so frequent flyer affinity points can be earned.

Whether a customer insists that their debit or check ATM card be used as a charge card, or if they explain that they forgot their PIN number, the retailer and eventually the consumer ends up paying for the banks' windfall profits.

[source: WayTooHigh.com]

If this is accurate, the credit card issuers are conditioning consumers to force retailers to pay substantially higher interchange fees. By using the allure of frequent flyer awards, the cardholders become Visa and MasterCard's moll to further enrich the multi-billion dollar interchange scheme. The banks promote the use of debit cards to help consumers budget their money, but the result is that merchants then are asked to process the card at much higher rates so frequent flyer affinity points can be earned.

Whether a customer insists that their debit or check ATM card be used as a charge card, or if they explain that they forgot their PIN number, the retailer and eventually the consumer ends up paying for the banks' windfall profits.

[source: WayTooHigh.com]

Thursday, March 02, 2006

Double-Digit Earnings at Citigroup Inc. and MasterCard International (WayTooHigh.com)

Profits at Citigroup Inc. soared to record levels in 2005 as the financial services company recorded a 44% increase in net income to nearly $25 billion. As more of a droll observation and pure coincidence, the widely reported annual merchant interchange revenues are also $25 billion.

MasterCard International also reported double-digit growth in 2005, with gross dollar volume rising nearly 12%.

Citigroup Inc. and MasterCard International are two of the named defendants in the payment card interchange fee antitrust litigation.

[source: WayTooHigh.com]

Motion To Name Lead Plaintiffs' Counsel (WayTooHigh.com)

Click on this link to view the Feb 24th Court order granting a motion to name the lead plaintiffs' counsel for the payment card interchange fee antitrust litigation.

Excerpt: As background, on June 22, 2005, Robins, Kaplan, Miller & Ciresi LLP acting as counsel for Photos, Etc. Corporation (30 Minute Photos Etc.), filed the first of some forty class action lawsuits brought to date on behalf of a class of merchants against the defendant credit card networks and certain of their member banks. In essence, the plaintiffs allege that the defendants have fixed transaction costs known as "interchange fees" at supracompetitive levels in violation of Section One of the Sherman Act. See DE 27 (Certain Class Plaintiffs' Memorandum of Law) at 1-2. By order of the Judicial Panel on Multidistrict Litigation dated October 19, 2005, that action and thirteen other related class action law suits brought in four separate districts were consolidated in the current litigation for pretrial purposes, and many more have since followed. See DE 2, DE 29, DE 94.

The Court appointed as the plaintiffs' co-lead counsel the following three law firms: Robins, Kaplan, Miller & Ciresi L.L.P.; Berger & Montague, P.C.; and Lerach, Coughlin, Stoia, Geller, Rudman & Robbins, L.L.P.

[source: WayTooHigh.com]

Excerpt: As background, on June 22, 2005, Robins, Kaplan, Miller & Ciresi LLP acting as counsel for Photos, Etc. Corporation (30 Minute Photos Etc.), filed the first of some forty class action lawsuits brought to date on behalf of a class of merchants against the defendant credit card networks and certain of their member banks. In essence, the plaintiffs allege that the defendants have fixed transaction costs known as "interchange fees" at supracompetitive levels in violation of Section One of the Sherman Act. See DE 27 (Certain Class Plaintiffs' Memorandum of Law) at 1-2. By order of the Judicial Panel on Multidistrict Litigation dated October 19, 2005, that action and thirteen other related class action law suits brought in four separate districts were consolidated in the current litigation for pretrial purposes, and many more have since followed. See DE 2, DE 29, DE 94.

The Court appointed as the plaintiffs' co-lead counsel the following three law firms: Robins, Kaplan, Miller & Ciresi L.L.P.; Berger & Montague, P.C.; and Lerach, Coughlin, Stoia, Geller, Rudman & Robbins, L.L.P.

[source: WayTooHigh.com]

Subscribe to:

Posts (Atom)