Saturday, September 30, 2006

Wednesday, September 27, 2006

MasterCard Rate Increase?! (WayTooHigh.com)

MasterCard® is actually preparing another assault on merchants and consumers. According to the NACS, they will again raise merchant interchange rates in mid-October.

It seems that little has changed.

Their plan is to increase World card rates on Oct 14th and the increase is widespread. We don't see any rates declining, but rising. Supermarkets are especially penalized. The new rates are increasing by about 4 percent at a time that our antitrust litigation should be causing pause.

The rate increases will apply to many cards, including: World Elite Standard, World Elite Key-Entered, World Elite Convenience, World Elite Supermarket, World Elite Warehouse, World Elite Public Sector, World Elite Restaurant.

[source: via NACS, WayTooHigh.com]

"Black Friday" (WayTooHigh.com)

We are wondering.

What would happen if on the day after Thanksgiving, on what is known as "Black Friday" - the busiest shopping day - when the credit card cartel is again poised to reap billions, if consumers demanded merchants process their debit cards as .... debit cards, rather than credit cards.

In drawing attention to the interchange fees, this campaign would canvas the nation with attention and raise more questions about the unbridled profiteering by Visa® and MasterCard®. Shoppers would signal they support their favorite stores. Rather than paying the banks a percent of every sale, retailers would then turn over a much smaller flat fee. The card association's are fighting back with contest gimmicks and promotions to force consumers to have stores swipe the cards at the much more costly credit card rates.

During the next few weeks we will explore how to promote and implement this plan.

[Commentary: WayTooHigh.com]

Saturday, September 23, 2006

Commentary on Technology, Fighting Mad Merchants and Real Blogs (WayTooHigh.com)

A newly invented silicon chip uses lasers, rather than wires to exponentially speed up information at a fraction of the cost. So, why is the credit card cartel initiating promotional gimmicks like caps on fill-up fees when motorists pay over $50 rather than lowering all rates due to advances in technology?

Is it greed, arrogance, or, just because they can?

Moore's Law of cost savings and technology efficiencies is one more reason why the $30 billion dollar annual interchange windfall forced upon consumers and merchants is infuriating many.

MERCHANTS ARE FIGHTING MAD

During an address to a Las Vegas photo industry conference this week, I heard from many retailers. Their concerns on interchange were interchangeable; each had stories about the fees and were all fighting mad. In all cases, their issues paralleled other retailers I hear from. They are mad as hell and not going to take it any more. One fellow attendee from Boston even mentioned the 1970s film Network and congratulated my partner and I as the very first lead plaintiffs for not just getting passionate, but taking action. I explained how the April, 2005 Wall Street Journal column (front page Marketplace) was partly the catalyst for leading us to become the personalities behind and foundation for this global battle.

His words and personal experience have become a new center piece in our personal battle with Visa®, MasterCard® and their member banks. No other person has ever expressed their appreciation for our role in filing the very first antitrust suit quit like him. He explained that after the horrors of September 11th, hearing stories about people standing up to injustice meant the world to him. His world profoundly changed on that day; his wife was on American Airlines' flight 11 and one of those lost on September 11th.

REAL BLOGS

We learned that the new hit NBC program 'Studio 60' had some technology marketing that was meant to appear as if fans of the show were hosting genuine blogs. Saturday's Los Angeles Times reported that the blog backfired because it was actually written by the network and underhandly was actually a "faux-blog." This is one more way corporate giants are designing unlevel playing fields, although the NBC faux blog was turned off hours ago and perhaps for good..

More about this example of a phony corporate blog from a Defamer.com blog posting:

While we found Defamer doppleganger Defaker, NBC's attempt to virally promote Studio 60 through a blog that seems to report gossip about the show's fictional universe in the form of interminably long episode summaries, an uncomfortably accurate commentary on our own half-assed efforts in the medium, we did unexpectedly discover something on the site to occupy our time: the open comments section of their inaugural post, a weird place where messages indulging the blog's premise (seemingly both from NBC staffers and people willing to play along with the joke), reviews of the show's pilot episode, opinions on the site's execution of its viral vision (verdict: try harder if you're going to bother), and general ragging on Amanda Peet's acting ability uncomfortably coexist. Here's a round-up of our favorite examples from the past couple of days:

Real people, real blogs and honest narratives will always beat out giant conglomerates' attempts to sway opinion. Just look at the credit card cartels efforts and compare it to WayTooHigh.com - The Credit Card Interchange Report. In their cases advocacy groups which enjoyed the financial support of Visa®, for instance, issued press releases and promoted the bank-owned views. Commentaries in newspapers also advocating their point of view must be measured by the people behind the curtain.[commentary: WayTooHigh.com]

Monday, September 18, 2006

Background News Items on 30 Minute Photos Etc. (Kiosk Market Place)

by James Bickers, editor • 18 Sep 2006 - Kiosk Market Place

When Fred Schwartz returned from a recent 16-day trip to Italy, the retired phone-company worker had a lot of pictures to print. As usual, he took his memory cards to 30 Minute Photos Etc.in his hometown of Irvine, Calif. But this time was different: Rather than hand the cards across the counter, Fred sat down at a photo kiosk and took matters into his own hands. He got hands-on assistance from storeowner Mitch Goldstone, plus some above-and-beyond treatment.

"Halfway through, he brings me cold bottled water and a candy bar," he said. "I’ve never been exposed to anyone helping out the customer that much, the extra step. I’m just not used to that kind of personalized service."

30 Minute Photos is indicative of an emerging trend where photo retailers use self-service in tandem with extraordinary customer service to create an atmosphere where people want to linger. Call it the "Starbucks effect."

"I’m using his services more and more," Schwartz said. "It’s just so comfortable in his store."

Catering to ‘Jennifer’

The proliferation of digital cameras has been good news and bad news for photo retailers — more people are taking more pictures, but they’re also printing them at home in large number. The Photo Marketing Association International reports that 61 percent of the digital photos printed in 2004 were done on home printers, versus 31 percent at retail. Retailers did better in 2005, but the majority of prints were still made at home.

"For the specialty photo retailer to survive, they have to clearly identify their target market and design an experience around that market," said Chad Munce, PMA’s group executive for digital-imaging markets. "If you consider the demographic of the memory-keepers in the household that are buying photographic products and services, you will see that the Generation X mom — PMA calls her ‘Jennifer’ — is the primary target for photo kiosk services."

Patrons use the DigiPrint Lounge at Dan's Camera City, Allentown, Pa.At Dan’s Camera City in Allentown, Pa., the experience is clearly aimed at Jennifer. The store’s 450-square-foot "DigiPrint Lounge" features 15 kiosk stations, each featuring a custom-designed stool, purse hooks and a La-Z-Boy chair for friends and family. A children’s entertainment area is nearby, and staffers are on hand with free coffee and other drinks. The lighting in the entire area is reduced, cutting down on glare on the Lucidiom kiosks.

"Customers — especially women — seek out the lounge," said Michael Woodland, chief executive of Dan’s. "It is relaxed, provides all they support they could wish for in terms of entertaining the kids, having a knowledgeable person at the ready, and easy-to-use systems."

Mitch Goldstone took a similar approach to 30 Minute Photos in June, when he remodeled the store to give it more of a boutique feel. "We redesigned the entire store — it was getting old-looking," he said. "There was a lot of clutter, and there wasn’t any of the type of merchandising and marketing that takes place in, say, a Starbucks. We wanted to create a unique destination experience, designed to make people stay and play."

At 30 Minute Photos in Irvine, Calif., a staffer teaches a customer to use the Lucidiom "Luci" kiosk.For 30 Minute Photos, that experience includes full-spectrum lighting, a high-end air filtration system, and a refrigerator full of Voss water and Ghirardelli chocolate — complimentary for customers.

"You go into the Ritz Carlton, for example, and they’ve always got fruit available at the front desk for their customers," he said. "That’s got a special magic to it, and we wanted that for our store."

The magic continues when customers leave, too — Goldstone said he hands out single-serving containers of Haagen-Dazs to departing shoppers. Goldstone said he couldn’t give specific revenue figures, but did say sales had risen 60 percent since June, when the store makeover took place.

"That’s an enormous number, especially when you consider that the traditional photo industry is down about 20 percent," he said. "We feel it’s extraordinary."

Paying more for the experience

"Why would anyone pay a dollar for a bookmark?" Steven Spielberg once asked. "Why not use a dollar as a bookmark?"

Spielberg’s frugal viewpoint underscores an aspect of human nature that is pivotal for retailers: the emotion of buying. In any given city, you can find a cup of coffee for a dollar or less. You also can find a $4 cup of coffee in that same town, very likely on the same block.

What justifies the difference? Taste and quality are part of it, but not all. Customers pay more for a positive buying experience, and interestingly, the phenomenon is not diminished with awareness — even if you know you’re paying way too much for coffee, you’ll occasionally do it anyway, because you enjoy it.

Dr. Michael Kasavana, professor of hospitality business at Michigan State University, said this phenomenon is well documented, and can be put to good use by the photo retail industry. "There is much research to indicate that a comfortable environment encourages more effective purchase decisions, and likely more spending," he said. "Additionally, a personal loyalty tends to be attached to the comfort station and hence a higher propensity for repeat business."

In the case of Dan’s Camera City, higher quality prints coupled with the "lounge experience" have justified higher prices — which customers are happily paying. "We are 29 cents for a 4-by-6," Woodland said. "That’s not a lot compared to other specialty stores, but certainly more than the local 19-cent big-box stores or the 9-cent online companies. In our case it is quality and experience. We do produce prints which are noticeably superior to these other sources, so there is a double incentive for them to choose us — allowing us to appeal to both the left and right side of their brain."

At 30 Minute Photos, prices used to hang on the walls. After the June makeover, they are nowhere to be found on the store signage. "Price isn’t an important component any longer," Goldstone said. "People are so dazzled with the service and quality that they don’t question the pricing."

[source: Kiosk Market Place]

Sunday, September 17, 2006

Thursday, September 14, 2006

70% of MasterCard's Board Now Independent (via AP)

[Source: via AP]

Tuesday, September 12, 2006

Is Visa® Taking Clarity and Replacing it with Hubris? (WayTooHigh.com)

Have you seen Visa U.S.A. Inc’s® print ad campaign and "Life Takes Visa®" slogan? (See sample: WSJ, Sept 12, p. B7).

The entire page in today's Wall Street Journal, for instance, contains tiny print to illustrate the complexity of traditional financial statements. Then the particulars: the copy explains that "Visa Business tracks your finances on one simple statement. So you can get your business’ financial story without reading between the lines. ... Your business is your life. Life takes Visa."

More factually, in our opinion, is that Visa® takes clarity and throws it out the window. On one hand, the world’s largest payment processing association promotes keeping it simple - then the fine print. For cardholders, the idea is to track finances with one simple statement, but for merchants, get out your detective’s hat and magnifying glass.

The typical merchant processing agreements are one-page, easy to follow forms. That is with the exception of the fine print. I had to zoom in so closely to the First Data Management Services® contract to find the hidden message, which was anything but simple. Look for yourself, request any merchant services company's processing agreement. What you will typically find is one sentence within the application and agreement that speaks volumes about how this game works.

Ex: "The client acknowledges having received and read a copy of the Interchange Schedule, Program Guide / Confirmation Page and Merchant Processing Application."

For merchants who sign on to accept electronic payments, for instance, there is hushed clarity followed by a multi, multi-paged, legal-ease appendix of non-simple-to-understand compliance; it is anything but fluent in simplicity.

Life might take Visa®, but for merchants accepting the cards, it could take seemingly a lifetime of reading and research to understand about interchange fees and how the leading payment processing association operates. Like the Visa® print ads, the contractual forms also have tiny print too which seems designed more to distract from this nearly 30 billion dollars in annual hidden taxes on retailers and consumers.

[Commentary: WayTooHigh.com]

"MasterCard Initiative: Priceless?" (Convenience Store News)

By Steve Holtz

PURCHASE, N.Y. -- A new initiative by MasterCard might save retailers a few bucks in the near future, but the company’s plan to establish a fee cap “of about $50 or more” for gasoline retailers won’t likely resolve the issues convenience store retailers face regarding credit card fees.

With a goal of “maximizing the value of MasterCard card acceptance,” Purchase, N.Y.-based MasterCard announced that it will soon implement the “significant interchange initiatives aimed at addressing concerns that have been raised by the merchant community,” the company said in a press release.

These initiatives include publishing all the MasterCard interchange rates that apply to U.S. merchants and establishing the cap on interchange fees on fuel purchases at petroleum retailers, a segment of the retail population that has been very vocal in contesting the fees at industry events and during congressional hearings, where antitrust concerns have been raised. A number of retail groups, including the National Association of Convenience Stores (NACS), have filed class-action suits against MasterCard, Visa USA and a number of major banks over interchange fees. The suits target the fees, which are paid by merchant banks to card-issuing banks. The merchants pay those fees indirectly as a component of fees charged to them by their banks.

“Consumers and merchants as well as MasterCard and its customers all benefit from a strong, competitive payments industry,” said Walt Macnee, president of the Americas for MasterCard. “One of my key goals is to enhance our ability to deliver value to merchants across the region.… Among the things merchants have told us they want is additional transparency around interchange rates and that because of the unique structure of the petroleum distribution business, gasoline retailers are disproportionately affected by high oil prices.”

Attempts to reach Bill Douglass, president of Douglass Distributing, and Hank Armour, NACS chairman, both of whom have testified before Congress on credit card issues, for comment on the initiatives were unsuccessful; however, it seems MasterCard is looking to smooth some rough edges in its relationship with retailers.

“We have heard the merchant concerns loud and clear,” said Joshua Peirez, group executive of global public policy for MasterCard. “We were the first in the industry to publish our merchant rules and procedures on our website, making them available free of charge or restrictions to any merchant who wants to access them. Merchants have since told us they would like us to publish our U.S. interchange rate schedule, and we are making a commitment to them that we will post the rates on our website on or before Nov. 1, 2006.

Peirez pointed out, however, that “interchange is only one component of the discount rate merchants pay for acceptance. Discount rates are set by the acquiring banks and independent service organizations that provide MasterCard acceptance to merchants. The merchant community believes that having access to our rate schedule will provide additional transparency to the process, so we are pleased to be able to accommodate their request.”

When published, the interchange rate schedule will be available at www.mastercardmerchant.com, where merchants can now access the MasterCard rules manual. The site also provides information to help merchants leverage card acceptance for their businesses.

“Similarly, merchants have told us that interchange fees on rapidly rising gasoline prices are a significant concern to them,” Peirez said. “MasterCard understands this concern. We believe that putting a cap on interchange fees when consumers use their MasterCard cards for gasoline purchases will benefit all gasoline retailers, as well as consumers who recognize that their purchases are faster and more convenient when they use their MasterCard cards at the pump. The cap will apply to consumer credit and debit cards and will provide benefits to gasoline retailers on credit-card transactions of about $50 or more. For example, on a $60 gasoline transaction, the reduction in interchange could be as much a 21%.”

“We have very few transactions that are over $50,” said Bill Walljasper, vice president and CFO of Casey’s General Stores, Ankeny Iowa.

Walljasper was asked about MasterCard’s new proposal, announced yesterday, during Casey’s quarterly earnings conference call. After noting “a 47% increase in credit card fees related to more expensive gasoline” compared to the previous year, Walljasper said simply, “Well over the majority of our transactions are below the $50 mark.... There’d have to be a substantial gas purchase to have that.”

Reacting to MasterCard’s moves, Visa said in an emailed statement to P-I News Services that there is "full visibility" within the company's pricing, adding that it will "continue to seek opportunities to increase clarity into all parts of our business and strengthen the organization's structure."

[Source: Convenience State News]

"Fewer Rewards for Those Who Buy" (The Baltimore Sun)

According to The Baltimore Sun, "Two major credit-card programs are preparing to scale back bonuses paid to consumers for gasoline and other purchases."

This raises the question of whether the credit card associations and member banks are also preparing to lower interchange fees.

Merchants already pay about one-hundred separate fees, including higher rates when cardholders choose affinity, rewards cards. As some banks are preparing to lower the award points for everyday purchases, will they just pocket the savings or refund it to retailers and consumers?

More transparency on Interchange Fee Schedules

And, what about posting U.S. merchant interchange fee schedules on the MasterCard® website beginning later this fall? What will happen as our overseas WayTooHigh.com readers see the website and respond? Many other industrialized nation's have much lower interchange rates and the transparancy will raise further questions about how these rates are established and its fairness.

[Source: WayTooHigh.com via The Baltimore Sun]

Monday, September 11, 2006

Revisiting the Merchant Interchange Complaint (WayTooHigh.com)

Among the nearly 500 previous WayTooHigh.com news and commentary postings, Visa® and MasterCard® make up much of the discussion. But, make no mistake, it is also the largest banks which we assert also unlawfully fix the fees charged to merchants for transactions

over their Visa® and Mastercard® Networks.

According to the amended complaint filing, their restrictions prevent merchants from protecting ourselves against these interchange fees. "Visa and Mastercard [pre-IPO] are not single entities; they are consortiums of competitors. They are owned and effectively operated by over 22,000 banks."

The merchant discount payment card interchange fee antitrust litigation includes several leading other defendants. From time to time we want to remind our readers of who the other defendants are as well; each are also member banks of the Visa® and Mastercard® networks.

As identified in the complaint filing, "many of the bank defendants are, or were during the relevant period, represented on the Visa and or Mastercard Boards of Directors at the times when those Boards collectively fixed uniform Interchange fees and imposed the anticompetitive anti-steering restraints and merchant restraints, tying and bundling arrangements, and exclusive-dealing. ...The bank defendants delegated to the Visa and Mastercard Boards of Directors the authority to take those actions. Each of the bank defendants had actual knowledge of, participated in, and consciously committed itself to the conspiracies..."

Listing of additional banking defendants:

Bank of America, N.A®

MBNA America Bank, N.A®

Barclays Bank Limited®

Capital One Bank®

Chase Bank USA®

Citibank N.A®

Fifth Third Bancorp®

First National Bank of Omaha®

National City Corporation®

SunTrust Banks, Inc®

Texas Independent Bancshares, Inc.®

Wachovia Bank, N.A.®

Washington Mutual, Inc.®

Providian National Bank®

Wells Fargo & Company®

[Commentary: WayTooHigh.com, background from the amended complaint filing]

Saturday, September 09, 2006

A Pause: Fifth Year Memorial (WayTooHigh.com)

from Aug 19, 2006]

from Aug 19, 2006]Years prior to the merchant interchange class-action antitrust litigation, we lead other advocacy campaigns.

Background: beyond co-editing WayTooHigh.com - The Credit Card Interchange Report and our business operations, several of our local and national campaigns to promote commerce and support important causes were forged from the events of September 11, 2001. That day fueled extraordinary emotions on a global scale. Rather than just watching the horrors of the day, we responded with a project to boost economic patriotism.. It was founded in Irvine, California, so we named it EPICC: Economic Patriotism in Irvine and Coast to Coast.

As native New Yorkers, the following two months were invested in bringing thousands of American's to New York City on Veteran's Day (November 11, 2001) to support the Big Apple, commerce and the airlines.

To view a summary of this campaign which garnered national

media coverage, click here.

media coverage, click here. The following year, on September 11, 2002, as few people were flying, we created "Fly With Courage" and traveled from Barcelona to New York City to Los Angles and demonstrated that air travel was safe. The Los Angeles TV affiliate for ABC covered the return trip. Afterwards, we created "Support The Games" and traveled to Athens for the Summer Olympics when many were staying away.

Many of our grassroots campaigns relate to supporting commerce and human rights. We even took on the controversial musical rapper Eminem during a prior year's MTV Video Music Awards show.

Beyond the news items, like a feature in the August edition of Popular Photography, our company was even profiled in a national IBM ad campaign.

{kind=link}

But, as lead plaintiffs in the nation's largest antitrust litigation - representing millions of merchants - this is a new journey; one which we have been engaged in since April, 2005 and paying interchange fees since 1990.

With nearly 500 prior WayTooHigh.com posting, T

he Credit Card Interchange Report is providing a global reach to this multi-billion dollar issue that impacts all retailers and consumers.

he Credit Card Interchange Report is providing a global reach to this multi-billion dollar issue that impacts all retailers and consumers. Additional news items are available here.

[source: WayTooHigh.com, link to EPICCUSA]

Friday, September 08, 2006

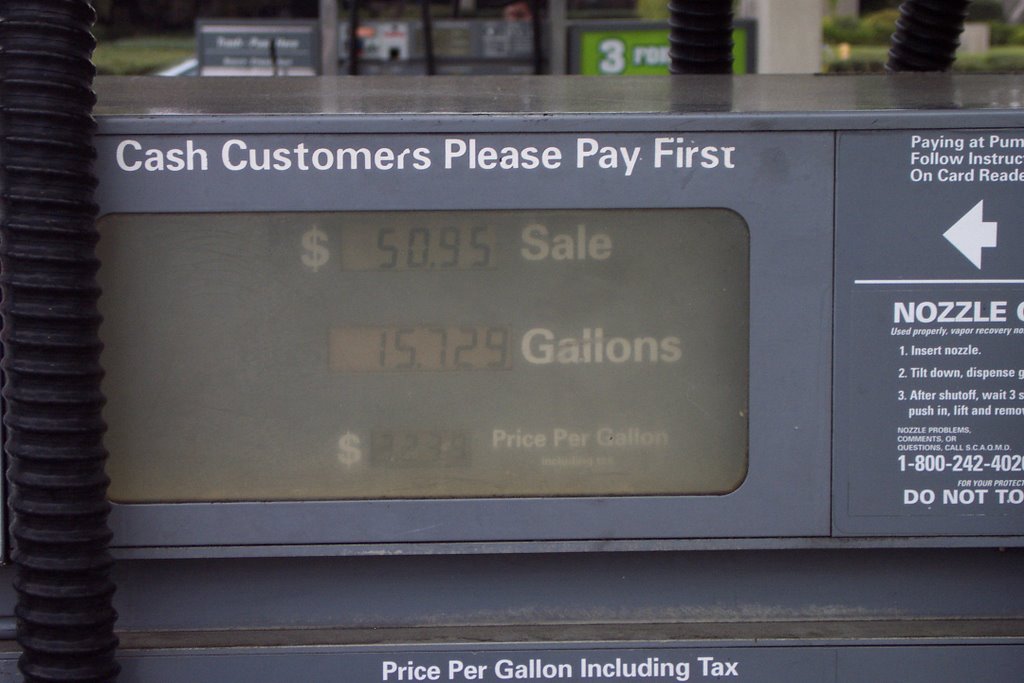

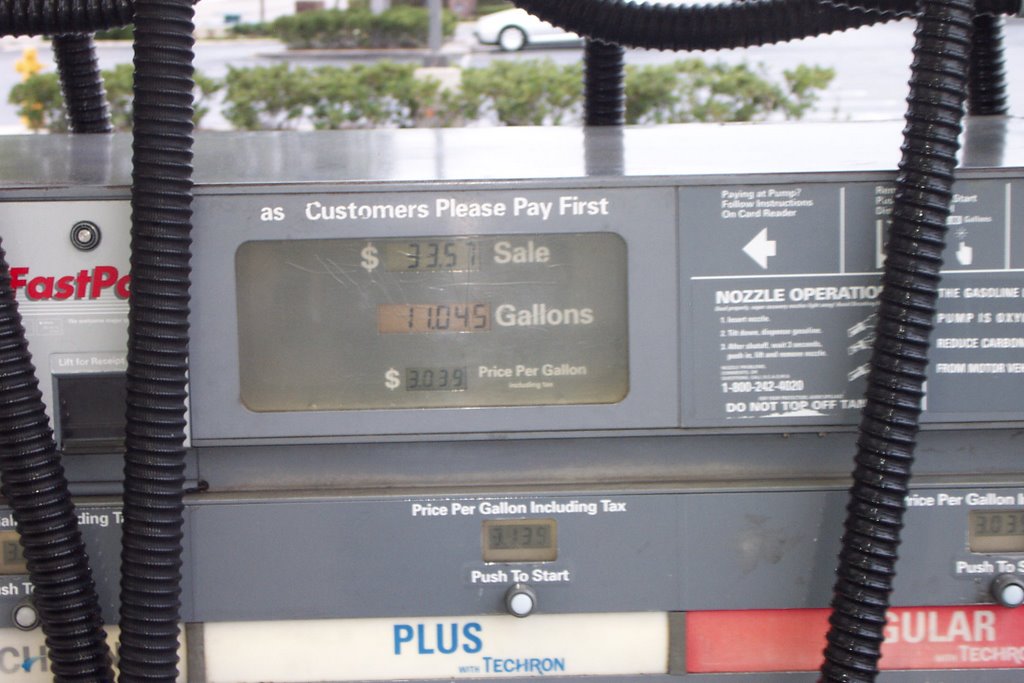

Giant Credit Card Cartels Answering Wrong Questions (WayTooHigh.com)

{kind=link}

On the surface, recent moves by the two largest credit card associations - which influence 80% of all electronic payment transactions - might aspire to soften merchant outrage. The recent solution by the second largest card association (posting interchange fee schedules and capping gas station interchange fees) is not very complex. But, it is little more than a distraction and watered-down bandage to placate the multibillion dollar interchange war.

MasterCard Worldwide's® press release might appear to signal an attempt to resolve the merchant concerns. However, from our prospective, it looks more like their Wizard of Oz handlers are driven by unseasoned publicists and muted marketing consultants. How else can their unabashed truculence justify the latest scheme to win over merchants and cardholders?

We randomly took pictures at our local service station this morning; in no case did any fill-ups cost more than fifty-dollars. This suggests that MasterCard's® latest concession to appease merchants is in our opinion, hollow. Even Visa® has been silent on matching this unreachable cap on fees at service stations.

We just went back and saw one pump total that was $50.75; which means, soon there will be no added interchange fee on ... 75-cents, what a sport!

Last fall we were profiled by the national media, including The Orange County Register and The Washington Post to draw attention to the windfall and unjustified profiteering waged by the card associations and member banks. A year later, as gas prices are easing off, MasterCard's® solution is (in our opinion) no solution, just more smoke and mirrors.

The other announced solution is to post the interchange fee schedules on Mastercard's® website. We hope it will be as simple to understand as McDonald's® posted nutritional information, then again, how many diners at the fast food chain actually read and understand those reports?

[Commentary: WayTooHigh.com]

Wednesday, September 06, 2006

"MasterCard Offers Concessions In Interchange Fee Battle" (ConsumerAffairs.com)

ConsumerAffairs.Com

September 6, 2006

The world's second-largest credit card company says it will publish a full schedule of the interchange fees merchants pay to process transactions using MasterCard-branded plastic. Visa indicated it had no immediate plans to match the move.

Separately, the credit card giant announced what it called a "partnership" with petroleum retailers to "cap off" the interchange fees charged when consumers fill up their tanks using credit or debit cards.

Walt Macnee, new president of MasterCard's American operations said the moves were designed to provide "additional transparency around interchange rates." "[B]ecause of the unique structure of the petroleum distribution business, gasoline retailers are disproportionately affected by high oil prices," he said.

The moves are widely seen as an attempt to appease merchants, in the face of class-action lawsuits led by merchant coalitions that claim MasterCard, Visa, and their partner banks collude to set artificially high interchange fees for merchants in order to boost their profits.

MasterCard set its fee cap for gas transactions for purchases of $50 or greater. Although the cap may be of benefit to owners of SUV's and truckers, the average motorist will still end up costing their merchant the full fee, particularly as gas prices continue to slowly drift under $3 a gallon.

Window Dressing

Retailer Mitch Goldstone, one of the leaders in the merchant lawsuits against the credit card companies, called the moves "window dressing."

Commenting on his blog, WayTooHigh.com, he said the move was akin to "enticing a diner at an all-you-can-eat buffet with a free dessert after their entire meal is finished."

Goldstone criticized the idea of publishing a fee schedule, saying consumers would be better served by an exact accounting of what the merchant pays to process different transactions, including food, clothes, and so on.

In an interview with ConsumerAffairs.Com, Goldstone questioned the timing of the move as well. "Why announce this now, after Labor Day? Did they already make all the money they needed to off vacationers?"

Goldstone has advocated much stronger transparency by credit card companies in terms of how their interchange fees work, and how much they really cost consumers and merchants alike. The merchant coalition claims that processing fees on plastic transactions can be so high that they wipe out any potential profit the retailers can make.

MasterCard's move can also be seen as an attempt to shed further risk in case of a successful outcome for the lawsuits. The credit card issuer recently went public, a move widely theorized to shift the potential costs of the lawsuits from member banks to investors.

Visa's Response

MasterCard's chief rival was relatively mum on the announcement of the fee publishing. Visa, which is still privately held, offered a statement saying that, "There is full visibility of pricing within the Visa system. Retailers do know, and always have known, the price they pay to accept Visa cards."

Goldstone remains skeptical that the two big credit card issuers are seriously differing on policy matters. "How can there be real competition when they're owned by the same banks and control 80 percent of the market?" he said.

[source: ConsumerAffairs.com]

"MasterCard Shares Rise on Merchant-Friendly Initiatives Possibly Aimed at Settlement" (AP)

Not so fast. MasterCard might consider these "merchant friendly initiatives" appeasing to retailers, but we see right through this newest scheme. Click here to read more.

[Source: WayTooHigh.com, news link via AP]

Tuesday, September 05, 2006

"Credit Card Break for Shell Dealers" (Convenience Store Decisions)

Shell Oil Products said it recognizes that the rising cost of gasoline is crushing fuel margins and it is offering its branded marketers a break.

To ease costs for its branded marketers, the Houston-based refiner-marketer has negotiated a permanent MasterCard merchant service fee reduction for its branded operators, effective immediately. The permanent fee is being reduced from 2.10% plus 10 cents to 2% plus 10 cents.

[source, abstract from Convenience Store Decisions]

"MasterCard Says to Disclose More Merchant Fees" (via Reuters)

After more than a year of drawing attention to our assertion that MasterCard®, Visa® and its member banks have colluded to illegally fix-prices, we are seeing some solid changes. However, any movements forward, such as Visa's® independent board and MasterCard Inc's® IPO deal with future changes. The antitrust litigation dates back over many years and involves billions of dollars.

Today, Reuters announced that MasterCard Worldwide® recognizes that its core customers are not pleased with the company and its practices. According to Reuters, the second largest credit card association will finally begin posting U.S. interchange fee rate schedules on its website. With nearly one-hundred separate fees, even with more transparency, retailers will find little comfort, as there are so many cards and fees that identifying the rates will still be a challenge.

WayTooHigh.com - The Credit Card Interchange Report had also reported on another solution of posting the exact interchange fee as part of each credit and debit card receipt.

MasterCard® appears to also be closely reading WayTooHigh.com and our assertions that they profiteered with windfall earnings as gas pump prices soared. Their solution: impose interchange fee pricing caps on fuel purchases. This is little more than window dressing, because the cap on its interchange fees are for fuel purchases of more than $50 at gas stations. Most motorists pay under that amount to fill up.

How will they resolve the years and billions of dollars in unbridled profiteering from our nation's record gas prices. The white flag was slightly raised and the cartel has been caught again. MasterCard® appears to be recognizing what many have questioned. Why should the banks' fees rise when gas prices rocketed upwards? To even an average consumer, this move suggests that the credit card cartels' have signaled that their fees are way too high.

This latest symbolic fix offers little more than enticing a diner at an all-you-can-eat buffet with a free dessert after their entire meal is finished. There is no room left, just like with most automobiles which get by with a fill-up under fifty-dollars.

Even publishing a complete list of interchange fees on the MasterCard® website provides about the same value as McDonald's® posting its ingredients online and at their stores. A better solution is to post the exact interchange fee on every cardholder's receipt. This way, fully transparent attention will be shared with merchants and cardholders so they understand more about this $30 billion dollar annual hidden tax and battle against the credit card associations and their member banks.

Questions:

What happens to those billions in previously paid service station interchange fees?

What about the other card association's participation? Will Visa® also cap their windfall profiteering or do more and rescind these fees?

[Commentary: WayTooHigh.com, news via Reuters]

Friday, September 01, 2006

"Those Hidden Fees" (Rochester Democrat and Chronicle )

(September 1, 2006) — When you withdraw cash from an ATM, you know upfront how much you're being charged for the convenience.With credit cards, the true cost is hidden in interchange fees that are charged to the retailer and then passed on to the customer in the form of higher prices. More light should be shined on this process.

With every transaction made by credit card, companies like Visa and MasterCard collect an interchange fee that averages about 1.8 percent of a purchase. It may be more or less depending on the size of the business.

Last year, credit card companies collected more than $30 billion in interchange fees from U.S. retailers. These fees are increasing.Credit card companies certainly deserve payment for their services, but there should be more transparency. The Federal Trade Commission does not require companies to disclose their interchange fees, and nearly all credit card contracts prevent retailers from showing the interchange fees on receipts. That makes it next to impossible for consumers to tell how much credit card purchases really cost, and customers who pay cash end up subsidizing credit card users.

Last year the U.S. House of Representatives passed a bill to get the Federal Trade Commission to analyze the effect of credit card interchange fees on gas prices. The Senate should do its part to make this happen. This kind of investigation is especially important in light of the more than 50 lawsuits that have been filed accusing Visa and MasterCard of colluding to keep their interchange fees high. Better regulation may be necessary.

Meantime, colleges that are offering financial literacy classes to help students avoid credit card debt should include information on interchange fees. More consumers should understand that the freebies credit card companies offer to get people to use their cards are actually driving prices up for everyone.

[source: Rochester D&C]